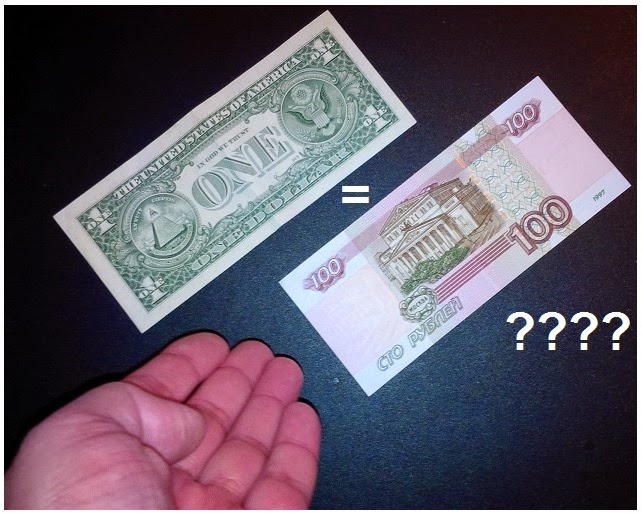

The Oilholic is feeling somewhat melancholy today! A crisp rouble note yours truly kept as a memento following a visit to Moscow in June is now worth considerably less when pitted against one’s lucky dollar!

At one stage over the past 24 hours, the US$1 banknote on the left was worth 79% of the RUB100 note on the right. One doubts whether a dollar would fetch a 100 roubles - but just putting it out there.

Barring a brief jump when the Russian government went for a free float of the currency back in November, there hasn’t been much to be positive about the rouble. Last evening’s whopper of an announcement by the Central Bank of Russia to raise interest rates by 650 basis points to 17% from 10.5% did little more than provide temporary respite.

Since January till date, Russia has spent has spent over $70 billion (and counting) in support of the rouble. Yet, the currency continues to feel the strain of escalating sanctions imposed by the West in tandem with a falling oil price.

However, there is a very important distinction to be made here. A falling oil price does not necessarily imply that Russian oil companies are in immediate trouble, repeat ‘immediate’ trouble. While a weak rouble makes imports costlier for the wider economy, which will almost certainly tip into a recession next year; oil – priced and exported in dollars - will get more ‘domestic’ bang for the converted bucks.

The Russian Treasury also adjusts tax and ancillary levies on oil exports in line with a falling (or rising) oil price. The policy is likely to keep things on a sound footing for the country’s oil & gas companies, including state-owned behemoths, for at least another 12 months.

How things unfold beyond that is anybody’s guess. First off, several Russian oil & gas players would need their next round of refinancing late next year or early on in 2016. With several international debt markets off limits owing to Western sanctions, the state will have to step in at least partially.

Secondly, the oil price is unlikely to stage a recovery before the summer, and would be nowhere near $100 per barrel. If it is still below $85 come June, as the Oilholic thinks it would be and the rouble does not recover, then corporate profits would take a plastering regardless of however much the Russian Treasury adjusts its tax takings.

Of course, not all in trouble would be Russian. Austrian, French and German banks with exposure to the country, accompanied by Russia-centric ETFs and Arctic oil & gas exploration will be hit hard.

Oil majors with exposure to Russia are already taking a hit. In particular, BP springs to mind. However, as the Oilholic opined in a Forbes article earlier this year - while BP could well do without problems in Russia, the company can indeed cope. For Total and Exxon Mobil, the financial irritants that their respective Russian forays have become of late would not be of major concern either.

Oil majors with exposure to Russia are already taking a hit. In particular, BP springs to mind. However, as the Oilholic opined in a Forbes article earlier this year - while BP could well do without problems in Russia, the company can indeed cope. For Total and Exxon Mobil, the financial irritants that their respective Russian forays have become of late would not be of major concern either.

Taking a macro viewpoint, market chatter about a repetition of the 1998 crisis is just that – chatter! Never say ‘never’ but a Russian default is highly unlikely.

Kit Juckes, global head of forex at Société Générale, says, “Comparisons with past crises – and 1998 in particular – are inevitable. The differences are more important than the similarities. Firstly, emerging market central banks (including and especially Russia) have vastly larger currency reserves with which to defend their currencies.

Kit Juckes, global head of forex at Société Générale, says, “Comparisons with past crises – and 1998 in particular – are inevitable. The differences are more important than the similarities. Firstly, emerging market central banks (including and especially Russia) have vastly larger currency reserves with which to defend their currencies.

“Secondly, US real Fed Funds are negative now, where they had risen sharply from 1994 onwards. That's a double-edged sword as merely the thought of Fed tightening has been enough to spark a crisis after such a long period of zero rates, but when the dust settles, global investors will still need better yields than are on offer on developed market bonds.”

The final difference, Juckes says, is that the rouble, in particular, is falling from a very great height in real terms. “It has only fallen below the pre-1998 peak in the last few days. It's still not cheap unless we believe that the gains in the last 16 years are all justified by productivity – an argument that works for some emerging market economies rather more than it does for Russia.," he concludes.

Finally, there is no disguising one pertinent fact in the entire ongoing Russian melee – the manifestly obvious lack of economic diversification with the country. Russia has remained stubbornly reliant on oil & gas exports and its attempts to diversify the economy seem even feebler than Middle Eastern sheikdoms of late.

For this blogger, the lone voice of reason within Russia has been former Finance Minister Alexei Kudrin. As early as 2012, Kudrin repeatedly warned of impending trouble and overreliance on oil & gas exports. Few Kremlin insiders listened then, but now many probably wish they had! That’s all for the moment folks! Keep reading, keep it ‘crude’!

To follow The Oilholic on Twitter click here.

To follow The Oilholic on Google+ click here.

To follow The Oilholic on Forbes click here.

To email: gaurav.sharma@oilholicssynonymous.com

© Gaurav Sharma 2014. Image: Dollar versus Rouble: $1 and RUB100 banknotes © Gaurav Sharma, 2014.

.jpg)