The decision or rather non-decision of not raising the OPEC production quota taken earlier here in Vienna is as damaging for OPEC as it is problematic. A cartel is supposed to show solidarity, but internal sparring awaited the world’s press. The meeting even concluded without a formal production decision or even a communiqué.

The decision or rather non-decision of not raising the OPEC production quota taken earlier here in Vienna is as damaging for OPEC as it is problematic. A cartel is supposed to show solidarity, but internal sparring awaited the world’s press. The meeting even concluded without a formal production decision or even a communiqué.It is clear now that those members in favour of a rise in production quota were Saudi Arabia, Kuwait, Qatar and UAE while those against were Algeria, Libya (Gaddafi’s lot), Angola, Venezuela, Iran and Iraq. However, majority of the sparring was between the Saudis on one side and the Iranians and Venezuelans on the other. In the end, it was not only messy but made the cartel look increasingly dysfunctional and an archaic union heading slowly towards geopolitical insignificance. However, what appears on the face of it is not so straightforward.

To followers of crude matters, it is becoming increasingly clear that as in the past, the Saudis will act to raise their production unilaterally, more so because they left Vienna irked by what they saw as Iranian and Venezuelan belligerence. Furthermore, the cartel’s own spare capacity of around 4 million b/d is squarely in the hands of Saudi Arabia, Kuwait and UAE. Of these, the Saudis pumped an extra 200,000 b/d last month. Most analysts expect this to be mirrored in their June output and it would imply that the Saudis would be producing at least 1 m b/d over the now largely theoretic OPEC binding quota of 24.85 million b/d.

Almost 41% of the global crude oil output is in the hands of OPEC. If within this close-knit group, there is sparring between those with spare capacity and those without in full view of the world’s press then the cartel’s central purpose takes a hammering. Mighty worried about the negative impact of high prices on GDP growth of their potential export markets and by default on the growth of crude oil demand, the Saudis appeared to the Oilholic to be firm believers that it was in their interest to increase quotas and actual production – so they will raise their own.

Yet I do not totally agree with market conjecture that the “end of OPEC is nigh”. Neither does veteran market commentator Jason Schenker of Prestige Economics. He notes: “Some market mavens have heralded this event as 'The end of OPEC' or 'The beginning of the end of OPEC', we do not believe it. Although no formal production decision was reached, there are precedents for what has been going on with the organisation’s production. After all, the group quota was suspended at the peak of the last business cycle in 2008.”

“Furthermore, and more recently, the individual member county quotas were suspended last October. On a more practical note, group cohesion for affecting production and crude oil prices is less critical when the price of crude is over US$100 per barrel and the global economy is rising, along with oil demand. The division within OPEC is likely to heal, and we are confident that group cohesion will be seen again when prices fall,” he concludes.

Additionally with half of those at the table being newcomers to the job, the situation in Libya and their representative, and an Iranian ‘acting’ oil minister with no experience of OPEC negotiations or of ‘crude’ affairs (he was previously the country’s minister for sport) all combined to complicate the situation as well as infuriate the Saudis. This situation should not arise at the next meeting.

Now if all this has left you yearning for a slice of OPEC’s history – whether you are an observer, derider or admirer of the cartel – there is no better place to start than Dr. Fadhil Chalabi’s latest book Oil policies, oil myths: Observations of an OPEC insider.

Now if all this has left you yearning for a slice of OPEC’s history – whether you are an observer, derider or admirer of the cartel – there is no better place to start than Dr. Fadhil Chalabi’s latest book Oil policies, oil myths: Observations of an OPEC insider.If there is any such thing as a ringside view of the wheeling and dealing inside OPEC then Dr. Chalabi more than anyone else had that view. The Oilholic found his book, which serves as the author’s memoir of his time at OPEC as well as charts the history of OPEC and its policies, to be a thoroughly good read.

He was the deputy secretary general of OPEC from 1979-89 and its acting secretary general from 1983-88. The book is, in more ways than one, a coupling of an account of his time at OPEC and an objective analysis of what has transpired in the energy business over last four decades. Looking through either prism - both the book's "memoir aspect" as well as the author's charting of the history of OPEC and its policies, it comes across as a thoroughly good read.

The book is just over 300 pages split by 16 chapters over which the author offers his thoughts in some detail about why OPEC is relevant. He also sets about exploding a few myths about the cartel, what has shaped it and how it has impacted the wider industry as well as the global economy.

To substantiate his case, he offers facts, figures, graphics, a glossary and a noteworthy and useful chronology of key events affecting the oil industry. The world has come a long way from the days when the “Seven Sisters” simply posted the oil prices in Platt’s Oilgram news bulletins. The era of price volatility-free cheap oil ended with the price shock of 1973 in the author’s opinion, before which the world had scarcely heard of OPEC.

Gaddafi’s Libya, Saddam’s Iraq and Nasser’s Egypt are all there but the Oilholic found Chapter 7 narrating the episode when Carlos the Jackal struck OPEC (in 1975) to be riveting, for among the hostages taken by the Jackal was the author himself. The book understandably has many fans at OPEC and officials from member nations as seen in its endorsements. However, what makes it enjoyable is that it is no glorification or advert of the cartel.

Rather it is an objective analysis of how crude oil has shaped the diplomatic relations of OPEC members with the oil-consuming nations globally and by default how an oil exporting cartel’s presence triggered ancillary developments in the crude business. This includes changing the investment perspective of IOCs who began facing dominant NOCs. In summation, if you would like to probe the supposed opacity of OPEC, Dr. Chalabi’s book would be a good starting point.

© Gaurav Sharma 2011. Photo 1: OPEC Flag © Gaurav Sharma 2011, Photo 2: Cover: Oil Policies Oil Myths © I.B. Tauris Publishers. Book available here.

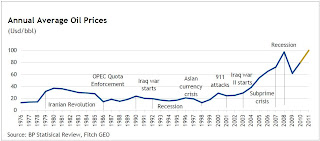

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)

It has been a month of quite a few interesting reports and comments, but first and as usual - a word on pricing. Both Brent crude oil and WTI futures have partially retreated from the highs seen last month, especially in case of the latter. That’s despite the Libyan situation showing no signs of a resolution and its oil minister Shukri Ghanem either having defected or running a secret mission for Col. Gaddafi depending on which news source you rely on! (Graph 1: Historical average annual oil prices. Click on graph to enlarge.)